Home » Posts tagged 'greenwashing'

Tag Archives: greenwashing

So what of social enterprises and the NHS? Corporate social responsibility and marketing revisited.

Milton Friedman’s famous maxim goes as follows:

“there is one and only one social responsibility of business – to use its resources and engage in activities designed to increase its profits so long as it stays within the rules of the game, which is to say, engages in open and free competition without deception or fraud.”

The history of social enterprise in fact extends as far back to Victorian England (Dart, 2004; Hines, 2005). The worker cooperative is one of the first examples of a social enterprise. Social enterprises prevail through- out Europe, and are most notable in the form of social cooperatives, particularly in Italy, Spain and increasingly France (Mancino and Thomas, 2005).

More recently, Clare Gerada, the Chair of the Royal College of General Practitioners, yesterday on BBC’s “The Daily Politics”, stated the following:

“Privatisation is the moving of State resources into the for full profit or non-profit sectors. And – the previous debate is that ‘if you don’t pay for therefore it’s not privatisation – it is privatisation. The profit that Specsavers or Harmoni make, they will not go back into the State: they will go straight into the shareholders.”

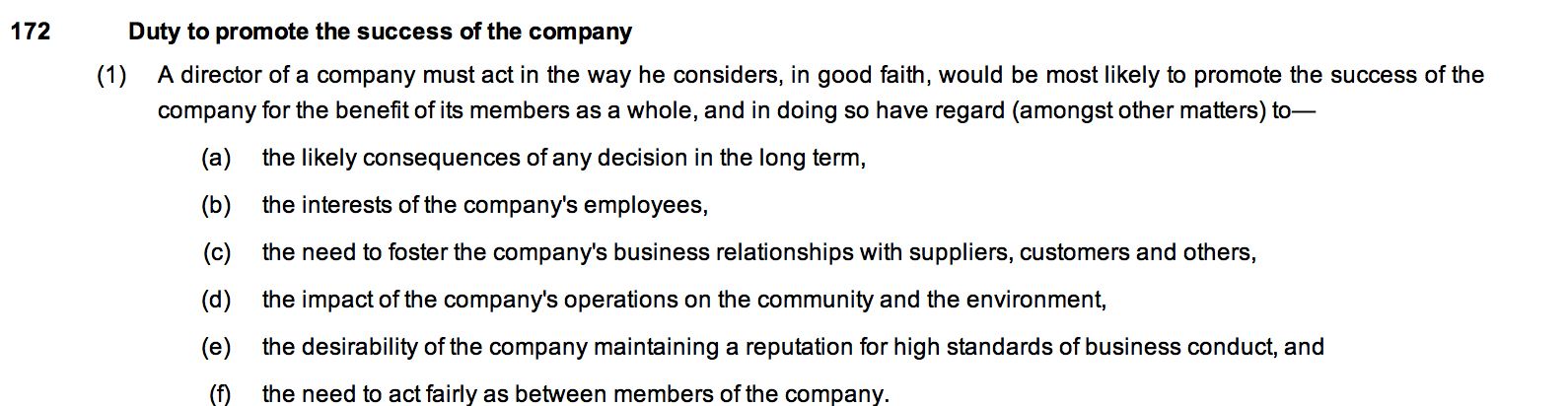

Currently, the position in English law is that the directors of every private limited company in law, whether they are called ‘social enterprises’ or not, have a statutory duty to the environment and stakeholders of their company. This is embodied in s.172 Companies Act (2006):

In an article by Rachel C. Tate, provocatively entitled, “Section 172 Companies Act 2006: the ticket to stakeholder value or simply tokenism?”, Tate argues as follows that stakeholder interests do not trump the interests of the company, i.e. to make profit. Interestingly. s.172 has no corollary in the common law.

“As highlighted, s172(1) formally obliges directors to consider stakeholder interests during the decision-making process. Yet, it is crucial to note that shareholder interests remain paramount. The interests of non-shareholding groups are to be considered only insofar as it is desirable to ‘(…) promote the success of the company for the benefit of its members.’17 A director will not be required to consider these factors beyond the point at which to do so would conflict with the overarching duty to promote company success. Stakeholder interests have no independent value in the consideration of a particular course of action.19 In addition, no separate duty or accountability is owed to the stakeholders included in the section.Thus, the duties of nurturing company success and having regard to the listed interests ‘(…) can be seen in a hierarchal way, with the former being regarded more highly than the latter.’21 Consequently, it would be wrong in principle to view s172 as requiring directors to ‘balance’ shareholders and stakeholder interests.22 These views are supported by industry guidance published on the effects of s172.”

“Social enterprises” are actually very hard to define. According to the United Kingdom (UK) government’s Department of Trade and Industry (2002), in the era of Tony Blair and Patricia Hewitt, a social enterprise is:

“a business with primarily social objectives whose surpluses are principally reinvested for that purpose in the business or in the community, rather than being driven by the need to maximise profit for shareholder and owners’”

Therefore, in theory, social ends and profit motives do not contradict each other, but rather have complementary outcomes, and constitute a ‘double bottom line’.

Nonetheless, the UK Government website contains a list of possible entities which could be described as ‘social enterprises’, namely:

- limited company

- charity, or from 2013, a charitable incorporated organisation (CIO is the new legal structure for charities)

- co-operative

- industrial and provident society

- community interest company (CIC)

- sole trader or business partnership

Note that in one of the vehicles, the limited company, as stated above, the primary duty of the directors is to promote success of the company. And that can be a “social enterprise”. Furthermore any contracts supplied to social enterprises can still still meet the definition of ‘privatisation’ above, not least because social enterprises are considered not to be wholly in the public sector (for example this EU definition, link here, where “Social enterprises are positioned between the traditional private and public sectors.”). Social enterprises do not meet the definition of what is typically in the public sector, by reference to the European System of Accounts 1995, link here. It is striking that the EU concede that one feature of social enterprises is a “significant level of risk”, so one has to question the long-term wisdom of competitive tendering contracts increasingly to social enterprises. Indeed, given that directors of English private limited companies are supposed to have due regard to wider “stakeholder” factors, one has to wonder quite what the point of the Public Services (Social Value) Act 2012 is. “Third Sector” magazine on 9 October 2012 reported that this enactment was not going that well:

“The Public Services (Social Value) Act could end up as a missed opportunity and more work needs to be done to encourage its use by commissioners and procurement professionals, delegates at the Labour Party conference heard. The act became law in March and places a duty on public bodies in England and Wales to consider “economic, social and environmental wellbeine in connection with public service contracts’! But at a fringe event hosted by the local infrastructure body Navca and the think tank ResPublica in Manchester, Hazel Blears, vice-chair of the All-Party Parliamentary Group on Social Enterprise, said she was concerned that many local authorities would not give it the attention it deserved.”The wording is weak,”she said.”If they had to ‘take account of social value, that would have been a harder position.””

There has been concern that in social enterprises, whilst the external environment may be given prominence, the internal environment may suffer (Cornelius et al., 2008):

“Since many social enterprises exist predominantly to address social ends (one key feature of the triple bottom line), it could be argued that the prevalence of their CSR policy and practice require close investigation. Emanuele and Higgins (2000) con- tribute to this agenda by challenging the assumption that non-profit organisations can offer comparatively lower wages, because they are more pleasant places to work. The authors emphasise that employees in this sector are often second income earners, and therefore are less concerned with lower wages and reduced benefits more characteristic of the private sector. They highlight how the voluntary sector is often a job entry point for new employees, who later move on to other sectors offering more fringe benefits, better financial security and healthcare programmes. They conclude with the assertion that ‘‘we must begin to exert the same pressure for ‘corporate responsibility’ among non-profit employers, as we demand in the private sector’’ (Emanuele and Higgins, 2000: 92), implying that the social enterprise sector needs to treat its employees better. Distinguishing between external and internal CSR may be beneficial, with social enterprises clearly focusing upon serving communities and overlooking crucial internal human resource issues.”

Grimsby “Care Plus” has been, in fact, highly commended in the UK Social Enterprise Awards (link here). The national competition, organised by Social Enterprise UK, recognises excellence in Britain’s growing social enterprise sector. And yet it was recently reported that, “More than 800 staff employed by the Care Plus Group – which provides adult health and social care across North East Lincolnshire – are in consultation over cuts to their pay and conditions.” Lance Gardner, the Chief Executive of the organisation, is reported as saying, “There is a lot of goodwill here. Our staff go that extra mile for their patients and have a passion for caring. They would not want to see them suffer. I do not want to take our goodwill for granted.”

The story of what happened between UNISON and Circle Hinchingbrooke is of course well known now (link here):

“Christina McAnea, head of health at Unison, said Circle could “cream off nearly 50% of the hospital’s surpluses” which would make it “virtually impossible to balance the books”.

“This is a disgrace. Any surpluses should be going directly into improving patient care or paying off the hospital’s debt, securing its future for local people – not ploughed into making company profits.

“Instead patients and staff are facing drastic cuts. The hospital was already struggling, but the creep in of the profit motive means cuts will now be even deeper. And it is patients and staff that will pay the price.””

Of course, ‘corporate social responsibility’ (“CSR”), abbreviated to ‘people, planet, profit’ somewhat tritely, has clashed before with marketing, so it is no wonder that businesses should wish to look ‘socially responsible’ to seek competitive advantage. Corporates have long been criticised for using diversity as a marketing ploy, e.g. putting in their promotional literature photos of employees in wheelchairs to demonstrate they are disabled-friendly. Pitches from social enterprises are likely to come with them ‘a feel good factor’ in competitive tendering, and of course any pitch which complies with adding social value in keeping with the new legislation is perfect “rent-seeking” fodder. But at the end of the day they are a range of entities seeking to make money which does not necessarily get fed back into frontline care, but used to generate a surplus aka profit. In an outstanding essay by Anna Kim for the 8th Ashbridge Business School MBA award, the author writes:

“Many critics believe that most of so-called CSR activities are nothing but a deceptive marketing tool, such as greenwashing. Can British American Tobacco be a ‘responsible’ cigarette manufacturer? Is Nestle really moving towards social values, or simply trying to wash its image around the baby milk and other ethical issues by putting a Fairtrade label on its 0.2% of coffee product line? From the green policy of oil giants BP and Shell to the childhood obesity research fund of McDonald’s, the list of controversial CSR examples is not exhaustive.”

So what of social enterprises and the NHS – remember Milton Friedman and Clare Gerada….

References

Cornelius, N., Todres, M., Janjuha-Jivraj, J., Woods, A., and Wallace, J. (2008) Corporate Social Responsibility and the Social Enterprise, Journal of Business Ethics, 81, pp. 355–370.

Dart, R. (2004) The Legitimacy of Social Enterprise’, Nonprofit Management and Leadership ,14(Summer), pp. 411–424.

Department for Trade and Industry (2002) Social Enterprise: A Strategy for Success, available at http://www.seeewiki.co.uk/~wiki/images/5/5a/SE_Strategy_for_success.pdf .

Hines, F. (2005) Viable Social Enterprise – An Evaluation of Business Support to Social Enterprises’, Social Enterprise Journal, 1(1), pp. 13–28.

Mancino, A. and Thomas, A. (2005) An Italian Pattern of Social Enterprise: The Social Cooperative, Nonprofit Management and Leadership, 15(3), pp. 357–369.

So what of social enterprises and the NHS?

People, planet, profit

What of social enterprises and the NHS?

Milton Friedman’s famous maxim goes as follows:

“there is one and only one social responsibility of business – to use its resources and engage in activities designed to increase its profits so long as it stays within the rules of the game, which is to say, engages in open and free competition without deception or fraud.”

The history of social enterprise in fact extends as far back to Victorian England (Dart, 2004; Hines, 2005). The worker cooperative is one of the first examples of a social enterprise. Social enterprises prevail through- out Europe, and are most notable in the form of social cooperatives, particularly in Italy, Spain and increasingly France (Mancino and Thomas, 2005).

More recently, Clare Gerada, the Chair of the Royal College of General Practitioners, yesterday on BBC’s “The Daily Politics”, stated the following:

“Privatisation is the moving of State resources into the for full profit or non-profit sectors. And – the previous debate is that ‘if you don’t pay for therefore it’s not privatisation – it is privatisation. The profit that Specsavers or Harmoni make, they will not go back into the State: they will go straight into the shareholders.”

Currently, the position in English law is that the directors of every private limited company in law, whether they are called ‘social enterprises’ or not, have a statutory duty to the environment and stakeholders of their company. This is embodied in s.172 Companies Act (2006):

In an article by Rachel C. Tate, provocatively entitled, “Section 172 Companies Act 2006: the ticket to stakeholder value or simply tokenism?”, Tate argues as follows that stakeholder interests do not trump the interests of the company, i.e. to make profit. Interestingly. s.172 has no corollary in the common law.

“As highlighted, s172(1) formally obliges directors to consider stakeholder interests during the decision-making process. Yet, it is crucial to note that shareholder interests remain paramount. The interests of non-shareholding groups are to be considered only insofar as it is desirable to ‘(…) promote the success of the company for the benefit of its members.’17 A director will not be required to consider these factors beyond the point at which to do so would conflict with the overarching duty to promote company success. Stakeholder interests have no independent value in the consideration of a particular course of action.19 In addition, no separate duty or accountability is owed to the stakeholders included in the section.Thus, the duties of nurturing company success and having regard to the listed interests ‘(…) can be seen in a hierarchal way, with the former being regarded more highly than the latter.’21 Consequently, it would be wrong in principle to view s172 as requiring directors to ‘balance’ shareholders and stakeholder interests.22 These views are supported by industry guidance published on the effects of s172.”

“Social enterprises” are actually very hard to define. According to the United Kingdom (UK) government’s Department of Trade and Industry (2002), in the era of Tony Blair and Patricia Hewitt, a social enterprise is:

“a business with primarily social objectives whose surpluses are principally reinvested for that purpose in the business or in the community, rather than being driven by the need to maximise profit for shareholder and owners’”

Therefore, in theory, social ends and profit motives do not contradict each other, but rather have complementary outcomes, and constitute a ‘double bottom line’.

This is the EU definition (link here):

Social enterprises are positioned between the traditional private and public sectors. Although there is no universally accepted definition of a social enterprise, their key distinguishing characteristics are the social and societal purpose combined with an entrepreneurial spirit of the private sector. Social enterprises devote their activities and reinvest their surpluses to achieving a wider social or community objective either in their members’ or a wider interest.

However, they note that social enterprises have a “significant level of risk“. The fact that a ‘social enterprise’ is not a public body means that it lacks full accountability through legal mechanisms such as freedom of information requests or judicial review (provided time limits are observed), which is an issue that the law will have to confront at some stage; how amenable is the law to address questions of private companies forming essentially public functions?

Nonetheless, the UK Government website contains a list of possible entities which could be described as ‘social enterprises’, namely:

- limited company

- charity, or from 2013, a charitable incorporated organisation (CIO is the new legal structure for charities)

- co-operative

- industrial and provident society

- community interest company (CIC)

- sole trader or business partnership

However, a page from ‘Social Enterprise Scotland’ is much more helpful in describing the different entities, and what criteria might embrace all social enterprises (link here; ht: Martin Rathfelder @SocialistHealth). However, it should be noted that the approach of social enterprises in Scotland is not exactly the same as that in England. In England, a useful definition of what a “co-operative” is has provided by the Communities and Local Government Committee recently (link here), but the Committee interestingly note a ‘paralysis of decision-making’ if there are too many stakeholders with dissenting views (this will be a valid criticism of any organisation):

“A genuine co-operative model would draw together both the ‘consumers’ and ‘producers’ of public services, and enable the users of services to participate in service production and delivery. The reciprocity a public service co-operative offers to its consumers could generate tangible economic advantages at local level when the profits could be distributed amongst members as dividends and/or recycled back to the communities to support further public services, resulting in a sustainable accumulation of social and pecuniary capitals and substantially reduced reliance of citizens on state-funded models.”

Note that in one of the vehicles, the limited company, as stated above, the primary duty of the directors is to promote success of the company. And that can be a “social enterprise”. Furthermore any contracts supplied to social enterprises can still still meet the definition of ‘privatisation’ above, not least because social enterprises are considered not to be wholly in the public sector (for example this EU definition, link here, where “Social enterprises are positioned between the traditional private and public sectors.”). Social enterprises do not meet the definition of what is typically in the public sector, by reference to the European System of Accounts 1995, link here. It is striking that the EU concede that one feature of social enterprises is a “significant level of risk”, so one has to question the long-term wisdom of competitive tendering contracts increasingly to social enterprises. Indeed, given that directors of English private limited companies are supposed to have due regard to wider “stakeholder” factors, one has to wonder quite what the point of the Public Services (Social Value) Act 2012 is. “Third Sector” magazine on 9 October 2012 reported that this enactment was not going that well:

“The Public Services (Social Value) Act could end up as a missed opportunity and more work needs to be done to encourage its use by commissioners and procurement professionals, delegates at the Labour Party conference heard. The act became law in March and places a duty on public bodies in England and Wales to consider “economic, social and environmental wellbeine in connection with public service contracts’! But at a fringe event hosted by the local infrastructure body Navca and the think tank ResPublica in Manchester, Hazel Blears, vice-chair of the All-Party Parliamentary Group on Social Enterprise, said she was concerned that many local authorities would not give it the attention it deserved.”The wording is weak,”she said.”If they had to ‘take account of social value, that would have been a harder position.””

There has been concern that in social enterprises, whilst the external environment may be given prominence, the internal environment may suffer (Cornelius et al., 2008):

“Since many social enterprises exist predominantly to address social ends (one key feature of the triple bottom line), it could be argued that the prevalence of their CSR policy and practice require close investigation. Emanuele and Higgins (2000) con- tribute to this agenda by challenging the assumption that non-profit organisations can offer comparatively lower wages, because they are more pleasant places to work. The authors emphasise that employees in this sector are often second income earners, and therefore are less concerned with lower wages and reduced benefits more characteristic of the private sector. They highlight how the voluntary sector is often a job entry point for new employees, who later move on to other sectors offering more fringe benefits, better financial security and healthcare programmes. They conclude with the assertion that ‘‘we must begin to exert the same pressure for ‘corporate responsibility’ among non-profit employers, as we demand in the private sector’’ (Emanuele and Higgins, 2000: 92), implying that the social enterprise sector needs to treat its employees better. Distinguishing between external and internal CSR may be beneficial, with social enterprises clearly focusing upon serving communities and overlooking crucial internal human resource issues.”

Grimsby “Care Plus” has been, in fact, highly commended in the UK Social Enterprise Awards (link here). The national competition, organised by Social Enterprise UK, recognises excellence in Britain’s growing social enterprise sector. And yet it was recently reported that, “More than 800 staff employed by the Care Plus Group – which provides adult health and social care across North East Lincolnshire – are in consultation over cuts to their pay and conditions.” Lance Gardner, the Chief Executive of the organisation, is reported as saying, “There is a lot of goodwill here. Our staff go that extra mile for their patients and have a passion for caring. They would not want to see them suffer. I do not want to take our goodwill for granted.”

The story of what happened between UNISON and Circle Hinchingbrooke is of course well known now (link here):

“Christina McAnea, head of health at Unison, said Circle could “cream off nearly 50% of the hospital’s surpluses” which would make it “virtually impossible to balance the books”.

“This is a disgrace. Any surpluses should be going directly into improving patient care or paying off the hospital’s debt, securing its future for local people – not ploughed into making company profits.

“Instead patients and staff are facing drastic cuts. The hospital was already struggling, but the creep in of the profit motive means cuts will now be even deeper. And it is patients and staff that will pay the price.””

This, unsurprisingly, has led UNISON to warn of the potential dangers of enterprises, specifically (this link):

“Social enterprises have been heralded as a ‘third way’ between private and state provision, combining the innovation, entrepreneurship and flexibility associated with the former with the public ethos and public interest of the latter. For some the expansion of social enterprise into mainstream services is an important part of policies for moving away from the state’s role in directly providing services and will help to improve them. For others this leads to the fragmentation of service provision, the incursion of private sector providers, the undermining of unions and central bargaining and a likely reduction in the public accountability of those services.”

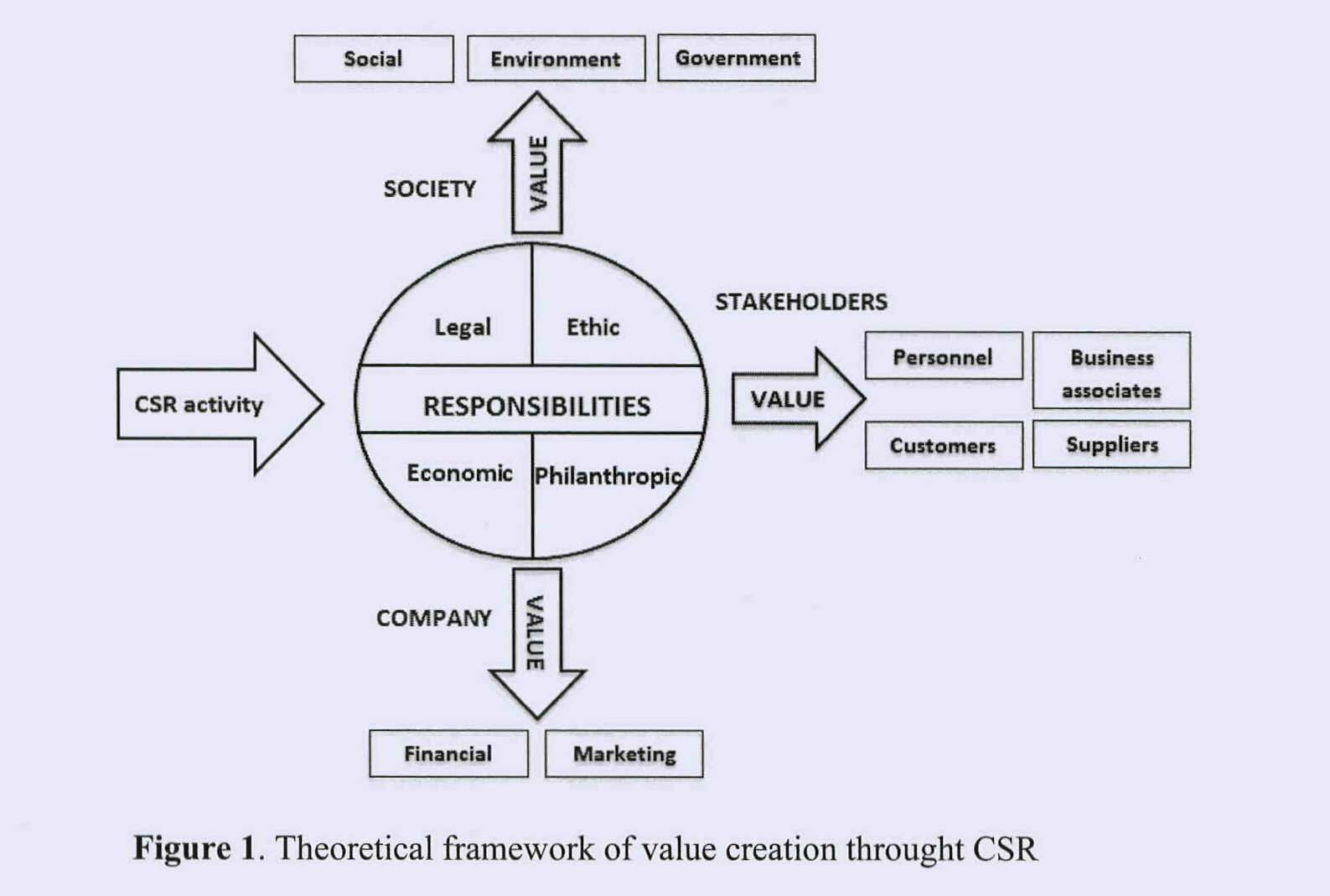

Of course, ‘corporate social responsibility’ (“CSR”), abbreviated to ‘people, planet, profit’ somewhat tritely, has clashed before with marketing, so it is no wonder that businesses should wish to look ‘socially responsible’ to seek competitive advantage. In the modern philosophy, of ‘value creation’, as discussed for example by Juscius and Jonikas (2013), value can only exist in the context of any company (whether called a “social enterprise” or not) in its wider environment. This is shown in the Fig. below.

FIG. Theoretical framework of value creation through CSR (details in text.)

Corporates have long been criticised for using diversity as a marketing ploy, e.g. putting in their promotional literature photos of employees in wheelchairs to demonstrate they are disabled-friendly. Pitches from social enterprises are likely to come with them ‘a feel good factor’ in competitive tendering, and of course any pitch which complies with adding social value in keeping with the new legislation is perfect “rent-seeking” fodder. But at the end of the day they are a range of entities seeking to make money which does not necessarily get fed back into frontline care, but used to generate a surplus aka profit. In an outstanding essay by Anna Kim for the 8th Ashbridge Business School MBA award, the author writes:

“Many critics believe that most of so-called CSR activities are nothing but a deceptive marketing tool, such as greenwashing. Can British American Tobacco be a ‘responsible’ cigarette manufacturer? Is Nestle really moving towards social values, or simply trying to wash its image around the baby milk and other ethical issues by putting a Fairtrade label on its 0.2% of coffee product line? From the green policy of oil giants BP and Shell to the childhood obesity research fund of McDonald’s, the list of controversial CSR examples is not exhaustive.”

So what of social enterprises and the NHS – remember Milton Friedman and Clare Gerada….

References

Cornelius, N., Todres, M., Janjuha-Jivraj, J., Woods, A., and Wallace, J. (2008) Corporate Social Responsibility and the Social Enterprise, Journal of Business Ethics, 81, pp. 355–370.

Dart, R. (2004) The Legitimacy of Social Enterprise’, Nonprofit Management and Leadership ,14(Summer), pp. 411–424.

Department for Trade and Industry (2002) Social Enterprise: A Strategy for Success, available at http://www.seeewiki.co.uk/~wiki/images/5/5a/SE_Strategy_for_success.pdf .

Juscius, V, Jonikas, D. (2013) Integration of CSR into value creation chain: conceptual framework, Inzinerine Ekonomika-Engineering Economics, 24(1), pp. 64-70.

Hines, F. (2005) Viable Social Enterprise – An Evaluation of Business Support to Social Enterprises’, Social Enterprise Journal, 1(1), pp. 13–28.

Mancino, A. and Thomas, A. (2005) An Italian Pattern of Social Enterprise: The Social Cooperative, Nonprofit Management and Leadership, 15(3), pp. 357–369.

Smell the Starbucks coffee: a toxic mix of marketing, politics and tax

In a page on the Starbucks website, Kris Engskov, Managing Director of Starbucks UK, Starbucks offered a full explanation. Engskov provided that, “I want to personally assure you that Starbucks pays and will continue to pay our share of taxes in the UK to the letter of the law. We always have and always will.” Meanwhile executives told analysts that the UK business was “successful”, “profitable” and they were “very pleased with the performance”. The company has made UK sales of £1.2bn in the past three years but declared no profit despite having described the British business as “profitable” to investors and analysts.

PayUpandGetOut, on the same webpage, offered a problem with this argument, “Yes, we know you’re paying “to the letter of the law”, but you are using the law to allow you to pay less tax than really you are expected to. It’s such a shame that you have worked so hard to improve your ethical credentials, and while this does not detract from your apprenticeships, links with local businesses and creation of more jobs, nor your support for farmers, it certainly makes me question your ethics, and thus will make me question buying from you in the future.” Some critics believe that corporate social activities are undertaken by companies such as British American Tobacco, BP, and McDonalds to distract the public from ethical questions posed by their core operations. They argue that some corporations start CSR programs for the commercial benefit they enjoy through raising their reputation with the public or with government. They suggest that corporations which exist solely to maximise profits are unable to advance the interests of society as a whole. Kappa99 offered another widely-held view that it is perfectly possible for somebody to act legally but totally immorally. Kappa99 writes, “Its legal to have sex with a horse in many US States. Its legal in the UK to kill a Scot in Nottingham with a crossbow.” There are numerous absurdities in how English law has evolved, to some extent through a process of ‘trial and error’.

Kris Engskov, UK managing director of Starbucks, has further added that the company had in the past three years “paid over £160 million in various taxes including National Insurance contribution for our 8,500 UK employees, and business rates”. Starbucks is not alone by any means. Last week it emerged that Facebook UK generated revenues of just £20.4m last year and paid just £238,000 in tax to the Revenue. Experts said the social networking giant was not breaking any rules but paid less tax because its European headquarters is not in the UK but in Ireland. Stephen Moss adds in the Guardian: “My mobile network is Vodafone, which UK Uncut alleges obtained a very favourable tax settlement that left £6bn in back taxes unpaid. The headache all these numbers are giving me will be salved by pills from Boots, another target for UK Uncut after moving its headquarters to Switzerland in 2008. In 2009-10, Boots paid just £14m on profits of £475m, equivalent to 3%.” Prominent tax campaigner Richard Murphy, from Tax Research UK, later in this article argues that, “Where there are alternatives we should look for them,” he says, “but we should also be clear that these actions are symbolic. The real purpose is getting political change.” Murphy says the objective should be to make corporate taxation more transparent and establish a ranking of companies – a sort of good corporate taxpayers’ guide. Margaret Hodge, chairman of the Public Accounts Committee, said HMRC should look at the company’s tax affairs after this Reuters report. MPs may also want to grill Starbucks’ management over the revelations. The PAC is responsible for scrutinising the stewardship of public funds, including tax collection.

However, Starbucks as a multi-national company does appear to take its environmental agenda seriously. Earlier this year, Starbucks announced the availability of EarthSleeve™, a new hot-cup sleeve that integrates proprietary technology that enables a reduction in overall material usage while at the same time increasing the post-consumer content. These adjustments correlate to a savings of nearly 100,000 trees. With nearly three billion* hot cup sleeves produced in the United States in 2011 and Starbucks representing nearly half of the marketplace, this material evolution will have a substantial impact on the packaging industry. In marketing management, there has been increasing interest in “greenwashing”. Starbucks, unlike other firms, does not appear to have been engaging in greenwashing activity, on the basis that it takes its environmental agenda seriously. Magali A. Delmas, a professor of management at the UCLA Institute of the Environment and Sustainability and the Anderson School of Management, in California Management Review (2011) has defined “greenwashing” as “a fixed and focus on firm communication about environmental performance … given the shorter time frame required for a firm to alter communications about its environmental performance than for a firm to change it, our analytical focus on the drivers that lead (some) firms to communicate positively about environmental performance while holding firm performance constant is not only useful for analytical tractability, but is also true to shorter-term strategic decisions of managers in these firms.”

There is no doubt that the social media is a major new influence in allowing consumers to give ‘instant feedback’ to suppliers. Indeed, as consumers, the public, and investors become more interested in environmental issues, environmental activist groups become more powerful and can exert more influence and pressure on companies. In the same way, now members of the public are able to give feedback about how they perceive far taxation might work. There is also no doubt in the past that corporates have been using their green credentials to secure “competitive advantage” in the marketplace, and there has been much interest latterly in how ethical banks could attract customers through a “competitive advantage” of acting ethically. George Osborne has a think-tank of a few lawyers thinking about how make the corporate tax system fairer. Taxation has clearly become an issue, with David Cameron restating in one breath that, “Fairness includes asking those on higher incomes to shoulder more of the burden than those on lower incomes. I’m not saying this is going to be easy, as we’ve seen with child benefit this week. But it’s fair that those with broader shoulders should bear a greater load”, while not pursuing aggressive tax policies in top earners.”

Meanwhile, Natalie Bennett, Green Party leader, in responding to David Cameron’s speech, provided that: “Further cutting the real rate of benefits, when they are already insufficient for a basic decent life is unconscionable. As the Joseph Rowntree Foundation calculated, the minimum weekly income needed in Britain is £193 for a single person, but out of work benefits deliver just £85.” A political party which is able to grasp the nettle of this complex toxic mix of marketing, politics and tax may reap dividends at the ballot box perhaps.